Abstract

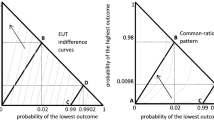

Betweenness is a weakened form of the independence axiom, stating that a probability mixture of two gambles should lie between them in preference. Betweenness is used in many generalizations of expected utility and in applications to game theory and macroeconomics. Experimental violations of betweenness are widespread. We rule out intransitivity as a source of violations and find that violations are less systematic when mixtures are presented in compound form (because the compound lottery reduction axiom fails empirically). We also fit data from nine studies using Gul's disappointment-aversion theory and two variants of EU, which weight separate or cumulative probabilities nonlinearly. The three theories add only one parameter to EU and fit much better.

Similar content being viewed by others

References

Allais, Maurice. (1953). “Le Comportement de L'homme Rationel Devant le Risque, Critique des Postulates et Axiomes de L'ecole Americaine.”Econometrica 21, 503–546.

Battalio, Ray C., John H. Kagel, and Jiranyakul Komain. (1990). “Testing Between Alternative Models of Choice Under Uncertainty: Some Initial Results,”Journal of Risk and Uncertainty 3, 25–50.

Becker, Gordon, Morris DeGroot, and Jacob Marschak. (1963). “An Experimental Study of Some Stochastic Models for Wagers,”Behavioral Science 3, 199–202.

Bernasconi, Michele. (1994). “Nonlinear Preference and Two-Stage Lotteries: Theories and Evidence,”The Economic Journal 104, 54–70.

Bordley, Robert. (1992). “An Intransitive Expectations-Based Bayesian Variant of Prospect Theory,”Journal of Risk and Uncertainty 5, 127–144.

Bordley, Robert, and Gordon Hazen. (1991). “SSB and Weighted Linear Utility as Expected Utility with Suspicion,”Management Science 37, 396–408.

Camerer, Colin F. (1989). “An Experimental Test of Several Generalized Utility Theories,”Journal of Risk and Uncertainty 2, 61–104.

Camerer, Colin F. (1992). “Recent Tests of Generalized Utility Theories.” In W. Edwards (ed.),Utility: Measurement, Theories, and Applications. Dordrecht: Kluwer Academic, pp. 207–251.

Chew, Soo-Hong, and Kenneth R. MacCrimmon. (1979). “Alpha-nu Choice Theory: An Axiomatization of Expected Utility,” Faculty of Commerce Working Paper No. 669, University of British Columbia.

Chew, Soo-Hong. (1983). “A Generalization of the Quasilinear Mean With Applications to the Measurement of the Income Inequality and Decision Theory Resolving the Allais Paradox,”Econometrica 53, 1065–1092.

Chew, Soo-Hong, and William S. Waller. (1986). “Empirical Tests of Weighted Utility Theory,”Journal of Mathematical Psychology 30, 55–72.

Chew, Soo-Hong. (1989). “Axiomatic Utility Theories With the Betweenness Property,”Annals of Operations Research 19, 273–298.

Chew, Soo-Hong, and Larry G. Epstein. (1990). “A Unifying Approach to Axiomatic Non-Expected Utility Theories,”Journal of Economic Theory 49, 207–240.

Chew, Soo-Hong, Larry G. Epstein, and Uzi Segal. (1991). “Mixture Symmetry and Quadratic Utility,”Econometrica 59, 139–163.

Chew, Soo-Hong, Edi Kami, and Zvi Safra. (1987). “Risk Aversion in the Theory of Expected Utility with Rank Dependent Probabilities,”Journal of Economic Theory 42, 370–381.

Conlisk, John. (1987). “Verifying the Betweenness Axiom With Questionnaire Evidence, or Not: Take Your Pick,”Economics Letter, 25, 319–322.

Coombs, Clyde, and Lily Huang. (1976). “Tests of the Betweenness Property of Expected Utility,”Journal of Mathematical Psychology 13, 323–337.

Cox, James, Vernon L. Smith, and James M. Walker. (1983). “A Test That Discriminates Between Two Models of the Dutch-first Auction Non-isomorphism,”Journal of Economic Behavior and Organization 4, 205–219.

Crawford, Vincent P. (1988). “Stochastic Choice with Quasiconcave Preference Functions.” University of California-San Diego Department of Economics Working Paper.

Crawford, Vincent P. (1990). “Equilibrium Without Independence,”Journal of Economic Theory 50, 127–154.

Debreu, Gerard. (1952). “A Social Equilibrium Existence Theorem,”Proceedings of the National Academy of Sciences 38, 886–893. Reprinted inMathematical Economics: Twenty Papers of Gerard Debreu. (1983). New York: Cambridge University Press.

Dekel, Eddie. (1986). “An Axiomatic Characterization of Preference Under Uncertainty: Weakening the Independence Axiom,”Journal of Economic Theory 40, 304–318.

Epstein, Larry G., and Stanley E. Zin. (1989). “Substitution, Risk Aversion and the Temporal Behavior of Consumption and Asset Returns: A Theoretical Framework,”Econometrica 57, 937–969.

Epstein, Larry G., and Stanley E. Zin. (1991a). “Substitution, Risk Aversion and the Temporal Behavior of Consumption and Asset Returns: An Empirical Analysis,”Journal of Political Economy 99, 263–286.

Epstein, Larry G., and Stanley E. Zin. (1991b). “The Independence Axiom and Asset Returns,” Department of Economics, University of Toronto.

Fishburn, Peter. (1982). “Nontransitive Measurable Utility,”Journal of Mathematical Psychology 26, 31–67.

Fishburn, Peter. (1983). “Transitive Measurable Utility,”Journal of Economic Theory 31, 293–317.

Fishburn, Peter. (1988).Nonlinear Preference and Utility Theory. Baltimore: Johns Hopkins University Press.

Gigliotti, Gary, and Barry Sopher. (1993). “A Test of Generalized Expected Utility Theory,”Theory and Decision 35, 75–106.

Green, Jerry, and Bruno Jullien. (1988). “Ordinal Independence in Nonlinear Utility Theory,”Journal of Risk and Uncertainty 1, 355–387. (erratum in 2(1988), 119).

Gul, Faruk, and Otto Lantto. (1990). “Betweenness Satisfying Preferences and Dynamic Choice,”Journal of Economic Theory 52, 162–177.

Gul, Faruk. (1991). “A Theory of Disappointment Aversion,”Econometrica, 59 667–686.

Handa, Jagdish. (1977). “Risk, Probabilities, and a New Theory of Cardinal Utility,”Journal of Political Economy 85, 97–122.

Harless, David. (1992). “Experimental Tests of Quasi-Bayesian Generalizations of Expected Utility Theory,” Virginia Commonwealth University Department of Economics Working Paper.

Harless, David, and Colin Camerer. (in press). “The Predictive Utility of Generalized Utility Theories,”Econometrica.

Hey, John and Chris Orme. (in press). “Investigating Parsimonious Generalizations of Expected Utility Theory Using Experimental Data,”Econometrica.

Kahneman, Daniel, and Amos Tversky. (1979). “Prospect Theory: An Analysis of Decision Under Risk,”Econometrica 47, 263–291.

Karmarkar, Uday S. (1978). “Subjective Weighted Utility: A Descriptive Extension of the Expected Utility Model,”Organizational Behavior and Human Performance 21, 61–72.

Karni, Edi, and Zvi Safra. (1989a). “Ascending Bid Auctions with Behaviorally Consistent Bidders,”Annals of Operations Research 19, 435–446.

Karni, Edi, and Zvi Safra. (1989b). “Dynamic Consistency, Revelations in Auctions and the Structure of Preferences,”Review of Economic Studies 56, 421–434.

Kreps, David M., and Evan L. Porteus. (1978). “Temporal Resolution of Uncertainty and Dynamic Choice Theory,”Econometrica 46, 185–200.

Kreps, David M., and Evan L. Porteus. (1979). “Temporal von Neumann-Morgenstern and Induced Preferences, ”Journal of Economic Theory 20, 81–109.

Lattimore, P.M., J.R. Baker, and A. Dryden Witte. (1992). “The Influence of Probability on Risky Choice,”Journal of Economic Behavior and Organization 17, 377–400.

Loomes, Graham, and Robert Sugden. (1987). “Some Implications of a More General Form of Regret Theory,”Journal of Economic Theory 41, 270–287.

Luce, R. Duncan. (1990). “Rational Versus Plausible Accounting Equivalences in Preference Judgments,”Psychological Science 1, 225–234.

Luce, R. Duncan. (1991). “Rank- and Sign-Dependent Linear Utility Models for Binary Gambles,”Journal of Economic Theory 53, 75–100.

Luce, R. Duncan, and Peter C. Fishburn. (1991). “Rank- and Sign-Dependent Linear Utility Models for Finite First-Order Gambles,”Journal of Risk and Uncertainty 4, 29–59.

Luce, R. Duncan, and Patrick Suppes. (1965). “Preference, Utility, and Subjective Probability.” In R.D. Luce, R.B. Bush, and E. Galanter (eds.),Handbook of Mathematical Psychology, Vol. 3. New York: Wiley, pp. 249–410.

Machina, Mark. (1982). “ ‘Expected Utility’ Analysis without the Independence Axiom,”Econometrica 50, 277–323.

Machina, Mark. (1985). “Stochastic Choice Functions Generated from Deterministic Preferences Over Lotteries,”Economic Journal 95, 575–594.

Machina, Mark. (1987). “Choice Under Uncertainty: Problems Solved and Unsolved,”Journal of Economic Perspectives 1, 121–154.

Machina, Mark. (1989). “Dynamic Consistency and Non-Expected Utility Models of Choice Under Uncertainty,”Journal of Economic Literature 26, 1622–1668.

Marschak, Jacob. (1950). “Rational Behavior, Uncertain Prospects, and Measurable Utility,”Econometrica 18, 111–141.

Prelec, Drazen. (1990). “A ‘Pseudo-endowment’ Effect, and its Implications for Some Recent Nonexpected Utility Models,”Journal of Risk and Uncertainty 3, 247–259.

Quiggin, John. (1982). “A Theory of Anticipated Utility,”Journal of Economic Behavior and Organization 3, 323–343.

Röell, Alissa. (1987). “Risk Aversion in Quiggin and Yaari's Rank-Order Model of Choice under Uncertainty,”Economic Journal 97, 143–159.

Schmeidler, David. (1989). “Subjective Expected Utility without Additivity,”Econometrica, 57 571–587.

Segal, Uzi. (1989). “Anticipated Utility: A Measure Representation Approach,”Annals of Operations Research 19, 359–373.

Segal, Uzi. (1990). “Two-stage Lotteries Without the Reduction Axiom,”Econometrica 58, 349–377.

Tversky, Amos, and Daniel Kahneman. (1986). “Rational Choice and the Framing of Decisions,”Journal of Business 59, S251-S278. Reprinted in R. Hogarth and M. Reder (eds.),Rational Choice: The Contrast between Economics and Psychology. (1987). Chicago: University of Chicago Press.

Tversky, Amos, Paul Slovic, and Daniel Kahneman. (1990). “The Causes of Preference Reversal,”The American Economic Review 80, 204–217.

Tversky, Amos, and Daniel Kahneman. (1992). “Advances in Prospect Theory: Cumulative Representations of Uncertainty,”Journal of Risk and Uncertainty 5, 297–323.

Viscusi, W. Kip. (1989). “Prospective Reference Theory: Toward An Explanation of the Paradoxes,”Journal of Risk and Uncertainty 2, 235–264.

Weber, Robert J. (1982). “The Allais Paradox, Dutch Auctions, and Alpha-utility Theory,” MEDS Department Discussion Paper No. 536, Northwestern University.

Weber, Martin, and Colin Camerer. (1987). “Recent Developments in Modelling Preferences Under Risk,”OR Spektrum 9, 129–151.

Wu, George. (1993). “Editing and Prospect Theory: Ordinal Independence and Outcome Cancellation,” Harvard Business School Managerial Economics Working Paper.

Yaari, Menahem E. (1987). “The Dual Theory of Choice Under Risk,”Econometrica 55, 95–115.

Author information

Authors and Affiliations

Additional information

The financial support of the National Science Foundation (SES 88-09299) is gratefully acknowledged. Comments from Larry Epstein, Rob Porter, John Quiggin, several anonymous referees, and seminar participants at the University of Pennsylvania were helpful.

Rights and permissions

About this article

Cite this article

Camerer, C.F., Ho, TH. Violations of the betweenness axiom and nonlinearity in probability. J Risk Uncertainty 8, 167–196 (1994). https://doi.org/10.1007/BF01065371

Issue Date:

DOI: https://doi.org/10.1007/BF01065371

Key words

- expected utility

- generalized utility

- risk-aversion

- prospect theory

- Allais paradox

- betweenness

- disappointment-aversion