How Covid Has Reshaped Real Estate From New York to Singapore

The retreat from major cities has been the pandemic’s big real-estate story — but that doesn’t mean metropolitan house prices have suddenly got cheap.

From New York to London to Sydney, ultra-low interest rates and vast government fiscal support have limited distressed sales. Still, apartment rents have plummeted and suburban bidding wars have erupted as millions of workers have learned they can work from anywhere.

“There’s been a spatial shock, whereby you don’t have to go to the city to earn money necessarily,” said Andrew Burrell, chief property economist at Capital Economics. “We think cities will change a lot.”

As vaccine rollouts allow more cities to tentatively reopen offices, bars, restaurants and museums, here’s a look at what’s changing — and what’s stayed the same.

Rents are where the Covid-19 effect is most obvious. Widespread job losses in fields like hospitality mean big groups of renters simply can’t afford to pay what they did previously. International students are gone. Young people have moved back in with parents.

And at the upper end of the market — where the biggest price falls have been — wealthier renters have opted not to stay in virtually closed cities.

While the price drops have stabilized, landlords are still having to offer steep discounts and perks to encourage people back. Which is an opportunity for some.

When it comes to buyers, whether mass-market or prestige, people want space. And many white-collar workers are prepared to bet they won’t have to be in the office full-time again. So areas that once seemed a little too far away — whether in the suburbs or even farther afield — are booming.

Vanguard estimates that around 30% to 40% of U.S. jobs — think bartenders or meat-packers — simply can’t be done remotely. At the other end of the spectrum, about 15% don’t need to go to a formal workplace at all. Most of these workers are higher-earning professionals like software developers or accountants.

It’s this second group — as well as those who fall somewhere in between, and who are not necessarily super rich but affluent — who can consider location arbitrage.

The gap between apartment and house prices has widened notably, although many analysts question how long that differential is sustainable.

“If they become cheap enough relatively, there is still demand for units,” Sarah Hunter, chief economist for BIS Oxford Economics, said. “House price growth won’t be able to outstrip unit price growth to the extent it currently is forever.”

Even as lockdowns have eased, mobility patterns in major cities are still way below the previous normal — especially for workplaces. For example in Sydney, where the successful containment of Covid-19 means a close-to-normal life is possible, city-center offices are still only about half full as new working patterns emerge.

For the past 30 years, property prices in global cities have largely raced ahead of their domestic markets. That dominant trend has now ruptured for the first time in decades.

So how permanent are these changing preferences?

Max Nathan, associate professor in Applied Urban Sciences at University College London, says that ultimately we won’t know whether “peak city” has passed until we see it in the rearview mirror. Much depends on whether vaccinations bring Covid-19 under control. For now though, the shift to the periphery and to what were previously considered second-tier cities is clearly happening.

In a few places, notably Ireland, authorities are trying to push the trend along. The Irish government said in late March it will create a network of remote working hubs and offer tax incentives for remote working.

“There are really signs that an intracity shift is happening,” Nathan said. “But we don’t know how far that’s going to go. We don’t quite know how far habits are going to swing back.”

London

By almost every metric, the pandemic’s hit to the allure of the U.K capital is clear. Rents in the smartest areas have been tumbling at the fastest annual pace in a decade.

At the top end of the market, brokers estimate luxury sales won’t recover for another five years, as those with cash to splash look for country piles rather than penthouses.

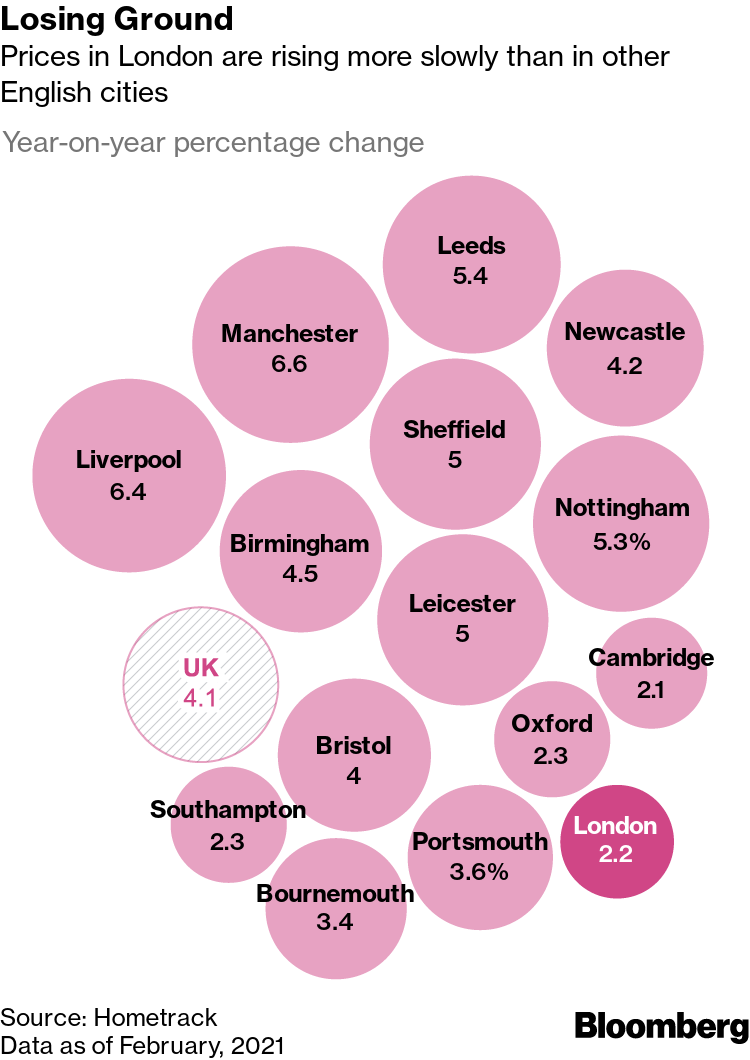

Losing Ground

Prices in London are rising more slowly than in other English cities

Data as of February, 2021

Source: Hometrack

In the mass market, the coastal county of Cornwall has replaced London as the U.K.’s most popular location for property searches — even though the capital city is about 16 times larger. London prices are rising, but at a rate that lags well behind other large English cities like Manchester or Birmingham.

“London seems to have been hit particularly badly,” Neal Hudson, founder of Residential Analysts, said. “It will recover but there probably will be some longer-term challenges. It’s perhaps not the growth story we’ve seen over the last 20 to 30 years that’s going to happen going forward.”

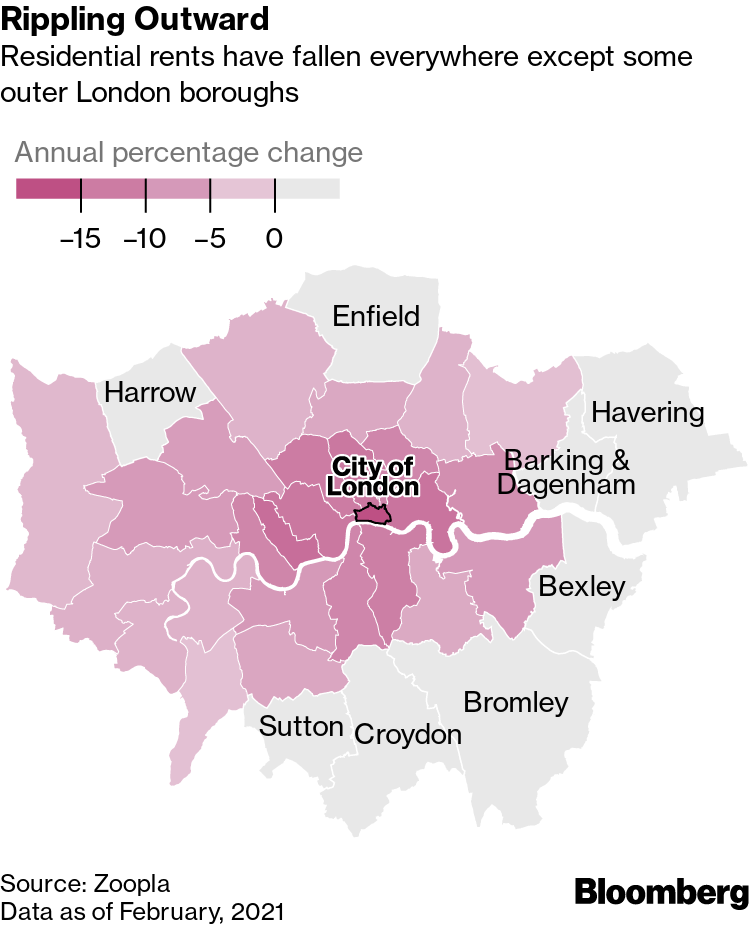

With some large U.K. employers including Standard Chartered Plc and Nationwide Building Society saying they will allow workers to do some days from home over the long term, it’s the outer boroughs that are in hot demand. While it hasn’t been this cheap to live in central London for almost a decade, average rents are rising further out.

Rippling Outward

Residential rents have fallen everywhere except some outer London boroughs

Data as of February, 2021

Source: Zoopla

Big houses in the picturesque southern countryside are seeing bidding wars. Young workers who could never hope to buy a home in the capital are looking elsewhere to discover what their money can buy in other cities such as Sheffield.

Almost one in four of those aged 18 to 44 who were surveyed by the Future Strategy Club said that they had permanently moved away due to the pandemic. Among 25- to 34-year-olds, the figure rose to 30%.

This burst of interest in places outside London may create its own problems, though, as new arrivals drive up prices.

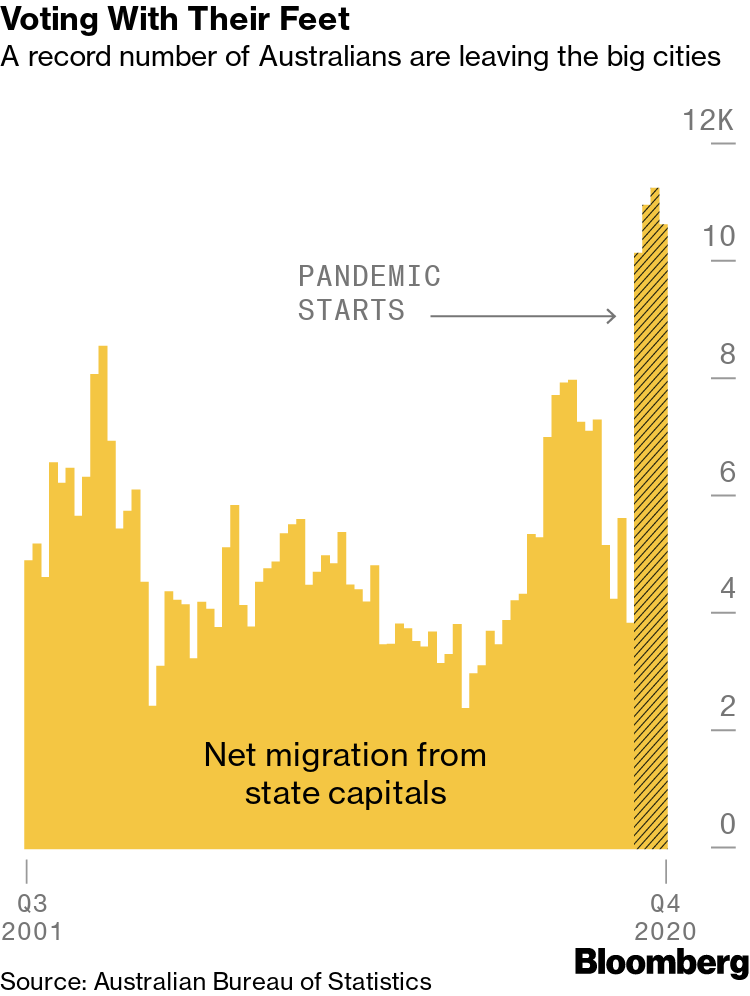

Sydney

If Australia’s financial capital is any guide, bringing the coronavirus under control isn’t enough on its own to prompt a return to the old normal.

With Covid-19 seemingly tamed in Sydney, there are few social-distancing restrictions and the musical “Hamilton” is playing to sold-out crowds. Yet the city is far emptier than it used to be.

Voting With Their Feet

A record number of Australians are leaving the big cities

Source: Australian Bureau of Statistics

The absence of international students and a new acceptance of at least some working from home means once sought-after city center apartments are cutting both asking prices and rents. By contrast, the suburbs are booming as a renewed fear of missing out sweeps the market.

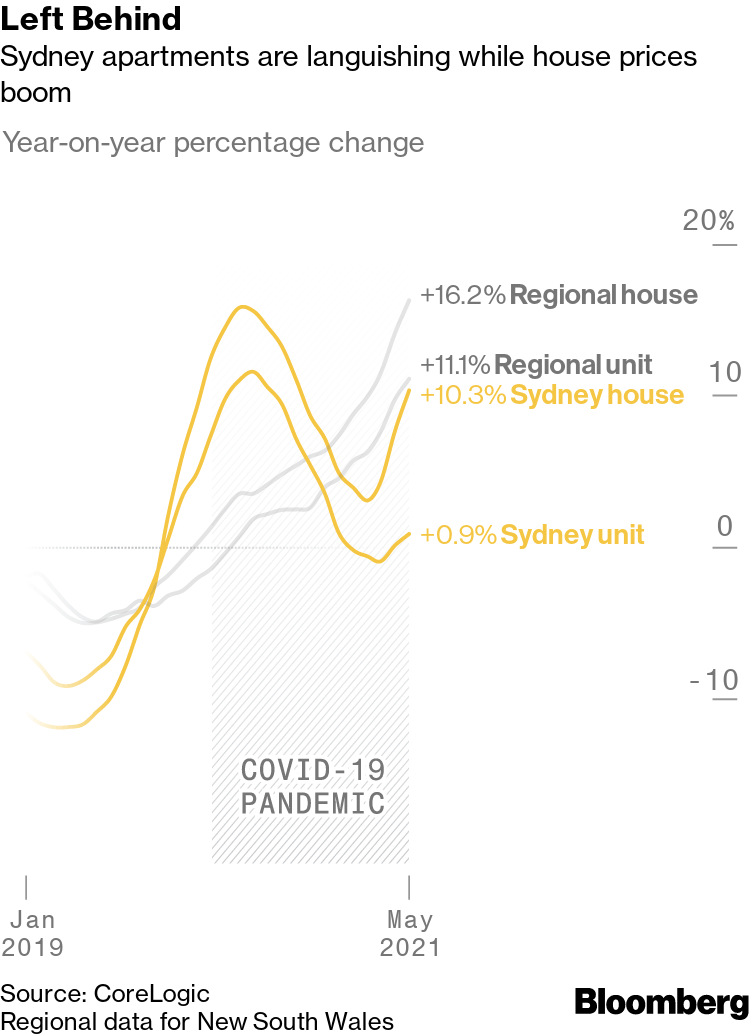

With listings numbers low, overall prices in Sydney are up 9.3% since the start of the year. Leading the charge have been detached houses in pricey suburbs close to the beach.

Even hotter are the state’s more rural areas where prices are up over 13% since last year. The key draw is lifestyle — and the possibility of buying the sort of large property with a garden that is increasingly only available in Sydney to the rich.

Left Behind

Sydney apartments are languishing while house prices boom

Regional data for New South Wales

Source: CoreLogic

Locations like Byron Bay, an upmarket holiday town nearly 500 miles north, saw prices surge 37% last year as wealthy Australians reassess where they want to spend their lives.

“Covid’s not the reason, it’s the catalyst,” said Tony Matthews, Senior Lecturer in Urban and Environmental Planning at Griffith University. “What’s changed is that people now have the ability to take a Sydney job with them.”

“It’s quite clear, though, it’s only an opportunity for certain people — mainly the white-collar affluent.”

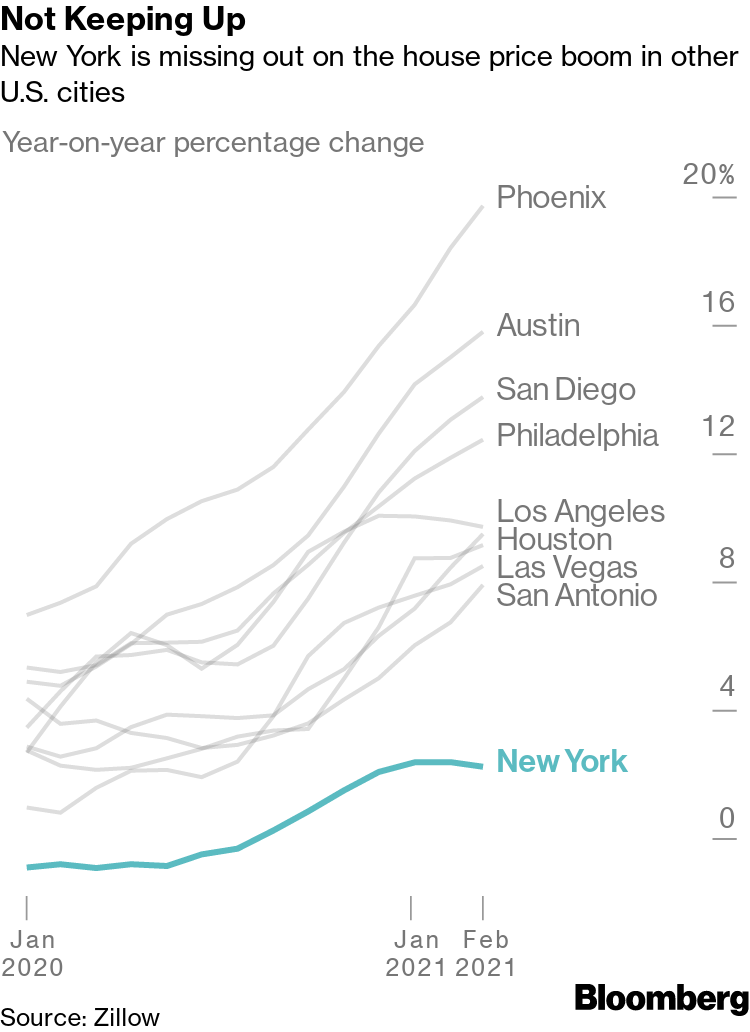

New York

Not Keeping Up

New York is missing out on the house price boom in other U.S. cities

Source: Zillow

For homebuyers looking to get the biggest discount in New York right now, the strategy is simple: Head to the areas with the largest number of office towers.

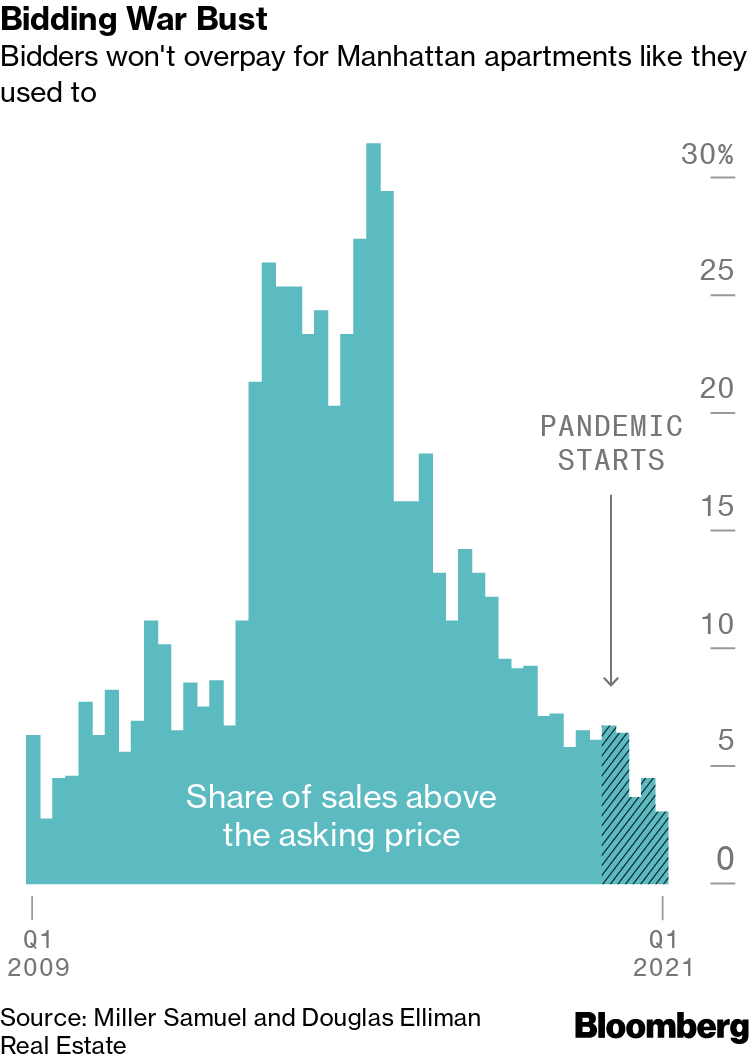

In Midtown East, vendors were forced to accept on average 14% below the asking price in the first quarter, according to brokerage Serhant. For Manhattan as a whole, 97% of condos sold at or below the asking price, a report from appraiser Miller Samuel Inc. and brokerage Douglas Elliman Real Estate found.

While there has been a slight uptick in apartment purchases, there’s no sign of a rush back. Instead, affluent workers are betting employers won’t force people back to the office full-time, despite prominent Wall Street banks like Goldman Sachs Group Inc. and JPMorgan Chase & Co. saying they’ll be encouraging people to return as soon as it’s safe.

Bidding War Bust

Bidders won't overpay for Manhattan apartments like they used to

Source: Miller Samuel and Douglas Elliman Real Estate

There’s also little sign that rental prices are set to increase anytime soon, with landlords in pricey areas forced to offer steep concessions. The soft rental market is offering people a chance to upgrade their living situations, and the number of new lease signings continues to soar each month as deal hunters move around in search of the best bargain.

But all that new lease activity isn’t putting a dent in the vacancy numbers. Last month there were nearly 20,000 empty rentals in Manhattan alone. And the fate of these units — for instance, how much they’ll rent for — depends heavily on how often people will be required to come to the office.

While there are signs that the dash to sunnier climes like Florida may have been over-hyped, the desire for space continues unabated even as the pandemic ebbs.

Thirty miles north of New York in leafy Westchester, where house prices soared in the early part of the pandemic, demand hasn’t slacked off. Sales of family homes were up 44% in the first quarter of 2021 compared with the same period last year.

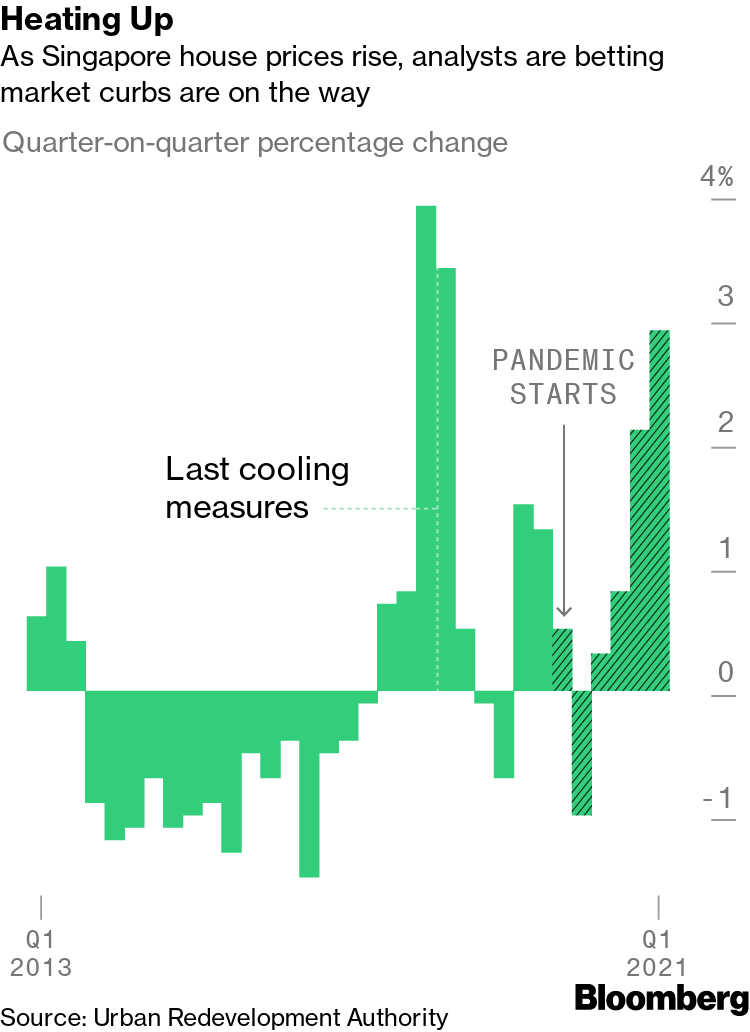

Singapore

There’s not much moving out to be done on an island that’s only 30 miles wide. Nor are there large country homes: Even at the top end of the market, most Singapore residents live in apartments.

Heating Up

As Singapore house prices rise, analysts are betting market curbs are on the way

Source: Urban Redevelopment Authority

So while agents report buyers looking for bigger apartments with better communal facilities (swimming pools and barbecue pits are standard in upmarket blocks), the picture isn’t anywhere near as dramatic as in other cities.

However, Singapore is in the middle of an upswing. Prices of private apartments are rising at the fastest pace since 2018, prompting speculation the government may step in to cool the market.

The momentum is widespread: A record number of former government flats are selling for over S$1 million ($743,000) and sales of private homes have reached the highest level in almost a decade.

The Million Club

A record number of Singapore public housing sales are netting over a million-dollars

Data summed quarterly

Source: SRX Property

Prices for bungalows — the Singaporean equivalent of a mansion — have also broken records. One such home sold recently for S$128.8 million, making it one of the most expensive in the city.

All this is happening even as foreign purchases have sunk to a 17-year low as expats return home and strict border controls remain.

Analysts see parents increasingly prepared to fund their children’s purchases as a key factor supporting demand.

“Parents could well be anxious about what the future may hold for their children, given rapid fire changes in technology and hence job security,” said Alan Cheong, executive director of research at Savills (Singapore) Pte. “Buying a private property for them could be seen as a partial hedge against the future economic uncertainties.”