Stock splits are events that increase the number of shares outstanding and reduce the par or stated value per share. For example, a 2-for-1 stock split would double the number of shares outstanding and halve the par value per share. Existing shareholders would see their shareholdings double in quantity, but there would be no change in the proportional ownership represented by the shares (i.e., a shareholder owning 1,000 shares out of 100,000 would then own 2,000 shares out of 200,000).

Stock splits are events that increase the number of shares outstanding and reduce the par or stated value per share. For example, a 2-for-1 stock split would double the number of shares outstanding and halve the par value per share. Existing shareholders would see their shareholdings double in quantity, but there would be no change in the proportional ownership represented by the shares (i.e., a shareholder owning 1,000 shares out of 100,000 would then own 2,000 shares out of 200,000).

Why would a company bother with a stock split? The answer is not in the financial statement impact, but in the financial markets. Since the same company is now represented by more shares, one would expect the market value per share to suffer a corresponding decline. For example, a stock that is subject to a 3-1 split should see its shares initially cut in third. But, holders of the stock will not be disappointed by this share price drop since they will each be receiving proportionately more shares; it is very important to understand that existing shareholders are getting the newly issued shares for no additional investment outlay. The benefit to the shareholders comes about, in theory, because the split creates more attractive opportunities for other future investors to ultimately buy into the larger pool of lower priced shares.

Rapidly growing companies often have share splits to keep the per share price from reaching stratospheric levels that could deter some investors. In the final analysis, understand that a stock split is mostly cosmetic as it does not change the underlying economics of the firm.

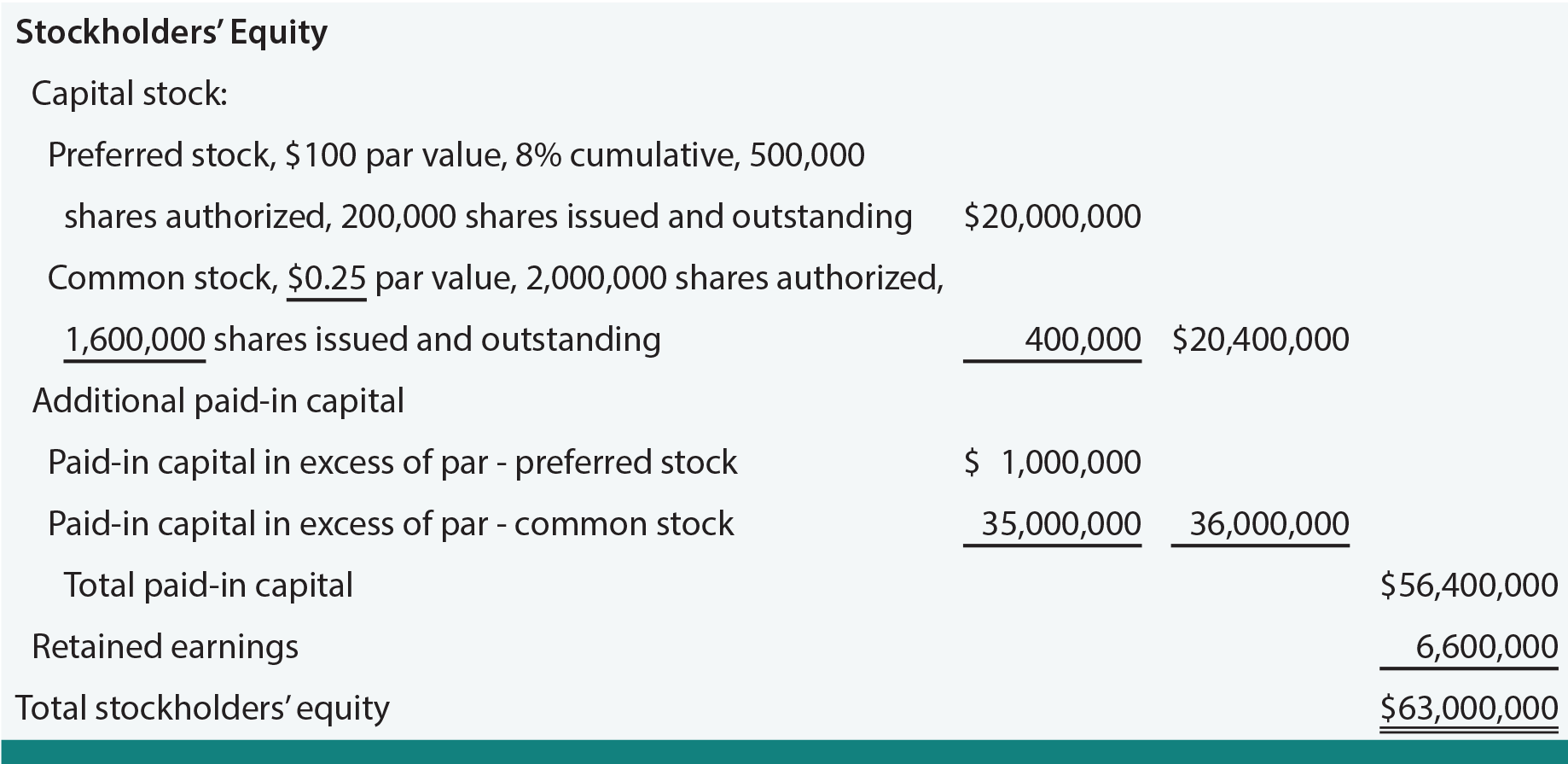

Importantly, the total par value of shares outstanding is not affected by a stock split (i.e., the number of shares times par value per share does not change). Therefore, no journal entry is needed to account for a stock split. A memorandum notation in the accounting records indicates the decreased par value and increased number of shares. If the initial equity illustration for Embassy Corporation was modified to reflect a four-for-one stock split of the common stock, the revised presentation would appear as follows (the only changes are underlined):

By reviewing the changes, one can see that the par has been reduced from $1.00 to $0.25 per share, and the number of issued shares has quadrupled from 400,000 shares to 1,600,000 (be sure to note that $1.00 X 400,000 = $0.25 X 1,600,000 = $400,000). None of the account balances have changes.

Splits can come in odd proportions: 3 for 2, 5 for 4, 1,000 for 1, and so forth depending on the scenario. A reverse split (1 for 5, etc.) is also possible and will initially be accompanied by a reduction in the number of issued shares along with a proportionate increase in share price.

Stock Dividends

In contrast to cash dividends discussed earlier in this chapter, stock dividends involve the issuance of additional shares of stock to existing shareholders on a proportional basis. Stock dividends are very similar to stock splits. For example, a shareholder who owns 100 shares of stock will own 125 shares after a 25% stock dividend (essentially the same result as a 5 for 4 stock split). Importantly, all shareholders would have 25% more shares, so the percentage of the total outstanding stock owned by a specific shareholder is not increased.

Although shareholders will perceive very little difference between a stock dividend and stock split, the accounting for stock dividends is unique. Stock dividends require journal entries. Stock dividends are recorded by moving amounts from retained earnings to paid-in capital. The amount to move depends on the size of the distribution. A small stock dividend (generally less than 20-25% of the existing shares outstanding) is accounted for at market price on the date of declaration. A large stock dividend (generally over the 20-25% range) is accounted for at par value.

Although shareholders will perceive very little difference between a stock dividend and stock split, the accounting for stock dividends is unique. Stock dividends require journal entries. Stock dividends are recorded by moving amounts from retained earnings to paid-in capital. The amount to move depends on the size of the distribution. A small stock dividend (generally less than 20-25% of the existing shares outstanding) is accounted for at market price on the date of declaration. A large stock dividend (generally over the 20-25% range) is accounted for at par value.

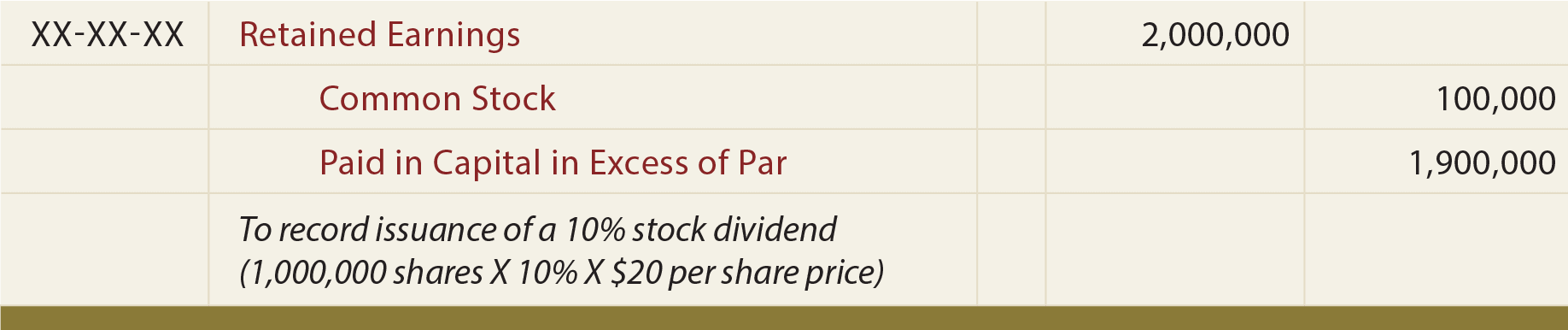

To illustrate, assume that Childers Corporation had 1,000,000 shares of $1 par value stock outstanding. The market price per share is $20 on the date that a stock dividend is declared and issued:

Small Stock Dividend: Assume Childers Issues a 10% Stock Dividend

Large Stock Dividend: Assume Childers Issues a 40% Stock Dividend

It may seem odd that rules require different treatments for stock splits, small stock dividends, and large stock dividends. There are conceptual underpinnings for these differences, but it is primarily related to bookkeeping. The total par value needs to correspond to the number of shares outstanding. Each transaction rearranges existing equity, but does not change the amount of total equity.

| Did you learn? |

|---|

| Differentiate between a stock split and a stock dividend, and the related accounting significance of each. |

| Know that journal entries are not needed for stock splits. |

| Understand the balance sheet modification necessitated by a stock split. |

| What is a stock dividend? |

| Be able to give reasons for issuing stock dividends. |

| Be able to prepare journal entries for small and large stock dividends, and cite examples of when each is appropriate. |

| Be able to provide computations demonstrating the impact of stock dividends on equity accounts. |

| Explain the probable impact on market value of stock splits and stock dividends. |